http://resources.thegospelcoalition.org/library/life-and-prosperity-death-and-destruction

47 minutes.

motivation vs. gospel preaching ;P

Deuteronomy Chapter 30 and etc.

"Love Him with all your heart and all your soul and live.

obey Him with your whole being in everything I am commanding you today."

Name-sake for this website is Deuteronomy 30:19 and 30:20

D3020.Blogspot.com (or http://www.ChooseLifeandLive.org)

Saturday, October 24, 2015

Wednesday, April 9, 2014

Yellen's March 31, 2014 speech and 18% on MMF.

What is your plan so you can take advantage of the good and avoid the bad?

Stagflation anyone? >_<

It may happen in 2015

and it happened in the late 1970s

where wage barely increased

but the interest rate went double digit in the 1980s.

[June 2015: well, a bit of deflation right now

but the minimum wage also rose to $10/hour in California]

30-year treasury bond with 13% interest.

18% interest on your money market account. yay~

10-12% on mortgage interest.

15-17% on car loan. boo~

- - - - - - - - -

She [Janet L. Yellen]

was sworn in as the head of Federal Reserve on February 3, 2014.

A speech was made on March 5th, 2014.

http://en.wikipedia.org/wiki/Janet_Yellen

Yeah~ From what I read, she's not the show-y type.

She is more of the boring-teacher type. :p

And with her fellow policymakers,

she has more than tons of work to do! -@.@-

She promised to keep the interest rate low until the unemployment improved,

which may go beyond 2015.

//The past six years have been difficult for many Americans... the hardships [job lost, sickness, etc] faced by some have shattered lives and families. Too many people know firsthand how devastating it is... [and] to run through your savings and even lose your home, as months and sometimes years pass.

The Fed provides this help by influencing interest rates. Although we work through financial markets, our goal is to help Main Street, not Wall Street. By keeping interest rates low, we are trying to make homes more affordable and revive the housing market. We are trying to make it cheaper for businesses to build, expand, and hire.

...

The other goal assigned by the Congress is stable prices, which means keeping inflation under control.

In the past, there have been times when these two goals conflicted--fighting inflation often requires actions that slow the economy and raise the unemployment rate. But that is not a dilemma now...

The Federal Reserve takes its inflation goal very seriously. One reason why I believe it is appropriate for the Federal Reserve to continue to provide substantial help to the labor market, without adding to the risks of inflation...

1)the seven million people who are working part time but would like a full-time job. This number is much larger than we would expect at 6.7 percent unemployment.

2) the decline in unemployment has not helped raise wages for workers as in past recoveries. Workers in a slack market have little leverage to demand raises.

3)extraordinarily large share of the unemployed who have been out of work for six months or more. These workers find it exceptionally hard to find steady, regular work, and they appear to be at a severe competitive disadvantage when trying to find a job.

4) an increasing share of the population is retired... But some "retirements" are not voluntary, and some of these workers may rejoin the labor force in a stronger economy. [some senior workers were force to retire when they cannot afford to do so, and need part-time job.]

//

http://www.federalreserve.gov/newsevents/speech/yellen20140331a.htm

At the 2014 National Interagency Community Reinvestment Conference, Chicago, Illinois

March 31, 2014

A comment from WallStreetJournal http://blogs.wsj.com/moneybeat/2014/03/31/janet-yellen-gives-one-of-the-most-dovish-speeches-i-have-ever-read/

Stagflation anyone? >_<

It may happen in 2015

and it happened in the late 1970s

where wage barely increased

but the interest rate went double digit in the 1980s.

30-year treasury bond with 13% interest.

18% interest on your money market account. yay~

10-12% on mortgage interest.

15-17% on car loan. boo~

What is your plan so you can take advantage of the good and avoid the bad?

Stagflation anyone? >_<

It may happen in 2015

and it happened in the late 1970s

where wage barely increased

but the interest rate went double digit in the 1980s.

[June 2015: well, a bit of deflation right now

but the minimum wage also rose to $10/hour in California]

30-year treasury bond with 13% interest.

18% interest on your money market account. yay~

10-12% on mortgage interest.

15-17% on car loan. boo~

- - - - - - - - -

She [Janet L. Yellen]

was sworn in as the head of Federal Reserve on February 3, 2014.

A speech was made on March 5th, 2014.

http://en.wikipedia.org/wiki/Janet_Yellen

Yeah~ From what I read, she's not the show-y type.

She is more of the boring-teacher type. :p

And with her fellow policymakers,

she has more than tons of work to do! -@.@-

She promised to keep the interest rate low until the unemployment improved,

which may go beyond 2015.

//The past six years have been difficult for many Americans... the hardships [job lost, sickness, etc] faced by some have shattered lives and families. Too many people know firsthand how devastating it is... [and] to run through your savings and even lose your home, as months and sometimes years pass.

The Fed provides this help by influencing interest rates. Although we work through financial markets, our goal is to help Main Street, not Wall Street. By keeping interest rates low, we are trying to make homes more affordable and revive the housing market. We are trying to make it cheaper for businesses to build, expand, and hire.

...

The other goal assigned by the Congress is stable prices, which means keeping inflation under control.

In the past, there have been times when these two goals conflicted--fighting inflation often requires actions that slow the economy and raise the unemployment rate. But that is not a dilemma now...

The Federal Reserve takes its inflation goal very seriously. One reason why I believe it is appropriate for the Federal Reserve to continue to provide substantial help to the labor market, without adding to the risks of inflation...

1)the seven million people who are working part time but would like a full-time job. This number is much larger than we would expect at 6.7 percent unemployment.

2) the decline in unemployment has not helped raise wages for workers as in past recoveries. Workers in a slack market have little leverage to demand raises.

3)extraordinarily large share of the unemployed who have been out of work for six months or more. These workers find it exceptionally hard to find steady, regular work, and they appear to be at a severe competitive disadvantage when trying to find a job.

4) an increasing share of the population is retired... But some "retirements" are not voluntary, and some of these workers may rejoin the labor force in a stronger economy. [some senior workers were force to retire when they cannot afford to do so, and need part-time job.]

//

http://www.federalreserve.gov/newsevents/speech/yellen20140331a.htm

At the 2014 National Interagency Community Reinvestment Conference, Chicago, Illinois

March 31, 2014

A comment from WallStreetJournal http://blogs.wsj.com/moneybeat/2014/03/31/janet-yellen-gives-one-of-the-most-dovish-speeches-i-have-ever-read/

Stagflation anyone? >_<

It may happen in 2015

and it happened in the late 1970s

where wage barely increased

but the interest rate went double digit in the 1980s.

30-year treasury bond with 13% interest.

18% interest on your money market account. yay~

10-12% on mortgage interest.

15-17% on car loan. boo~

What is your plan so you can take advantage of the good and avoid the bad?

Thursday, March 6, 2014

Choosing Life in the Midst of an Adverse Pregnancy - ProLife issue

http://www.focusonthefamily.com/radio.aspx?ID={C9A72745-8701-4B62-B20D-46988804E692}

Choosing Life in the Midst of an Adverse Pregnancy (Part 1 of 2)

Choosing Life in the Midst of an Adverse Pregnancy (Part 1 of 2)

In 2008, Angie Smith and her husband Todd (lead singer of the group Selah) learned through ultrasound that their fourth daughter had conditions making her “incompatible with life.” Advised to terminate the pregnancy, the Smiths chose instead to carry this child and allow room for a miracle. That miracle came the day they met Audrey Caroline and got the chance to love her for the precious two-and-a-half hours she lived on earth. The Smiths share the first part of their incredible story today on “Choosing Life in the Midst of an Adverse Pregnancy” –

Monday, October 7, 2013

D.I.M.E.

I was talking with friends couple weeks ago about the life insurance coverage at their work.

It turned out that the company covers up to 100K,

which is quite generous considering IRS says any company is not going to be able to deduct for coverage over 50K.

http://www.irs.gov/Government-Entities/Federal,-State-&-Local-Governments/Group-Term-Life-Insurance

So, is 100K enough?

It is certainly enough for a burial (~15K, not counting land plot) and cremation (~2K).

It is certainly not enough for to cover the 30-year mortgage for someone who purchased a house in OC within the last 5 years; or have children who are over the age of 10 and are planning to go to college.

D.I.M.E is a quick way to calculate the coverage needed.

D - Debt. Car loan, Credit Card Debt, etc.

[usually not applicable for Asian Americans I know. Being very politically-incorrect here.]

I - Income. Annual income multiplies by 20 years.

(or 10 years if the main income earner is retiring within the next 10 years.)

M - Mortgage. How much is left to pay?

It turned out that the company covers up to 100K,

which is quite generous considering IRS says any company is not going to be able to deduct for coverage over 50K.

http://www.irs.gov/Government-Entities/Federal,-State-&-Local-Governments/Group-Term-Life-Insurance

So, is 100K enough?

It is certainly enough for a burial (~15K, not counting land plot) and cremation (~2K).

It is certainly not enough for to cover the 30-year mortgage for someone who purchased a house in OC within the last 5 years; or have children who are over the age of 10 and are planning to go to college.

D.I.M.E is a quick way to calculate the coverage needed.

D - Debt. Car loan, Credit Card Debt, etc.

[usually not applicable for Asian Americans I know. Being very politically-incorrect here.]

I - Income. Annual income multiplies by 20 years.

(or 10 years if the main income earner is retiring within the next 10 years.)

M - Mortgage. How much is left to pay?

E - Education. How much student loans one have left to be paid off.

and/or how much you are saving for your children to go to college?

(p.s. State College tuition has tripled in the last 6 years.)

Usually, for a full-time worker, this number is no less than 1 million, even without the mortgage.

5-year term life insurance should be relatively cheap to start until the age of 40. That is why AAA loves to advertise it. Then it become expensive so most people have a hard time replacing the coverage when the 20- or 30- year term are over, which is when the family may need the coverage the most.

Frankly, the coverage could be significantly less when one re-calculate for the coverage sum through the DIME at age 55 rather than at age 22. On the other hand, a family of age 22-ers recovers much more readily than a family with age 55 single-income provider.

Talk to me if this does not make sense.

Sincerely,

Mindy

2013 October

and/or how much you are saving for your children to go to college?

(p.s. State College tuition has tripled in the last 6 years.)

Usually, for a full-time worker, this number is no less than 1 million, even without the mortgage.

5-year term life insurance should be relatively cheap to start until the age of 40. That is why AAA loves to advertise it. Then it become expensive so most people have a hard time replacing the coverage when the 20- or 30- year term are over, which is when the family may need the coverage the most.

Frankly, the coverage could be significantly less when one re-calculate for the coverage sum through the DIME at age 55 rather than at age 22. On the other hand, a family of age 22-ers recovers much more readily than a family with age 55 single-income provider.

Talk to me if this does not make sense.

Sincerely,

Mindy

2013 October

Friday, October 4, 2013

“I like your Christ....[but] Your Christians are so unlike your Christ."

Mindy's conclusion:

sometimes it is still easy for me [all human] to make

a 5-second judgement on others in this rushed world.

The graceful thought of this reflective and honest author

is simply TMI (too much information.)

I wish/pray non-Christians and different Christian

will both understand me when I act totally imperfect.

////

It is believed Mahatma Gandhi said, “I like your Christ,

I do not like your Christians.

Your Christians are so unlike your Christ."

Statements like these have been made millions of times,

and with good reason. Many of us live unlike Jesus.

... it makes sense that many feel this way.

Christians have done many awful things in the name of Jesus.

...why do we so quickly move to the place of ignoring our weaknesses

and pointing the finger at others?

We must be willing to own up to our own mistakes and the mistakes of others."

- -

We should admit we have been wrong, caused pain and

that we share in the guilt of misrepresenting Jesus.

...He went person-by-person through his office and apologized.

One of his co-workers who was the most cynical toward Christians said to him,

“I didn’t know Christians ever apologized. It’s good to finally hear it!”

- -

In my experience, people don’t expect Christians to be perfect.

Any time I have ever admitted my faults, no one has been surprised.

It turns out everyone already knows I am imperfect.

They have just been waiting for me to be honest about my imperfections.

Too often we criticize the behavior of others

and condemn the masses for their grave sin,

all the while ignoring our own sinful behavior.

[Christ's] heart broke for the sinners in the margins

and for the super religious who thought they were doing the right thing.

If I’m honest, I usually don’t

[ carry that type of compassion toward the zealots.]

Especially when it comes to judgmental, bigoted or legalistic Christians.

More often than not, I am just angry at how they treat others.

Mostly, I am frustrated because others associate me with them.

..if we are more honest and open about ourselves, we would see the log

in our own eyes, and know we have a lot of work to do on ourselves

before we can deal with the splinter in the eyes of our brothers and sisters.

And if we practice this kind of honesty and openness,

we then can speak about something else:

namely, the grace, love and transforming power of God.

It is then we can move from talking about all the bad things

Christianity has brought about and instead

talk about the good things Jesus has brought about.

** If this happens, we won’t need to tell anyone what we are not like,

because they will already know what we are like. **

////

~ ~ ~ ~ ~ ~ ~ ~

http://www.relevantmagazine.com/god/church/should-we-apologize-church

sometimes it is still easy for me [all human] to make

a 5-second judgement on others in this rushed world.

The graceful thought of this reflective and honest author

is simply TMI (too much information.)

I wish/pray non-Christians and different Christian

will both understand me when I act totally imperfect.

////

It is believed Mahatma Gandhi said, “I like your Christ,

I do not like your Christians.

Your Christians are so unlike your Christ."

Statements like these have been made millions of times,

and with good reason. Many of us live unlike Jesus.

... it makes sense that many feel this way.

Christians have done many awful things in the name of Jesus.

...why do we so quickly move to the place of ignoring our weaknesses

and pointing the finger at others?

We must be willing to own up to our own mistakes and the mistakes of others."

- -

We should admit we have been wrong, caused pain and

that we share in the guilt of misrepresenting Jesus.

...He went person-by-person through his office and apologized.

One of his co-workers who was the most cynical toward Christians said to him,

“I didn’t know Christians ever apologized. It’s good to finally hear it!”

- -

In my experience, people don’t expect Christians to be perfect.

Any time I have ever admitted my faults, no one has been surprised.

It turns out everyone already knows I am imperfect.

They have just been waiting for me to be honest about my imperfections.

Too often we criticize the behavior of others

and condemn the masses for their grave sin,

all the while ignoring our own sinful behavior.

[Christ's] heart broke for the sinners in the margins

and for the super religious who thought they were doing the right thing.

If I’m honest, I usually don’t

[ carry that type of compassion toward the zealots.]

Especially when it comes to judgmental, bigoted or legalistic Christians.

More often than not, I am just angry at how they treat others.

Mostly, I am frustrated because others associate me with them.

..if we are more honest and open about ourselves, we would see the log

in our own eyes, and know we have a lot of work to do on ourselves

before we can deal with the splinter in the eyes of our brothers and sisters.

And if we practice this kind of honesty and openness,

we then can speak about something else:

namely, the grace, love and transforming power of God.

It is then we can move from talking about all the bad things

Christianity has brought about and instead

talk about the good things Jesus has brought about.

** If this happens, we won’t need to tell anyone what we are not like,

because they will already know what we are like. **

////

~ ~ ~ ~ ~ ~ ~ ~

http://www.relevantmagazine.com/god/church/should-we-apologize-church

Monday, September 30, 2013

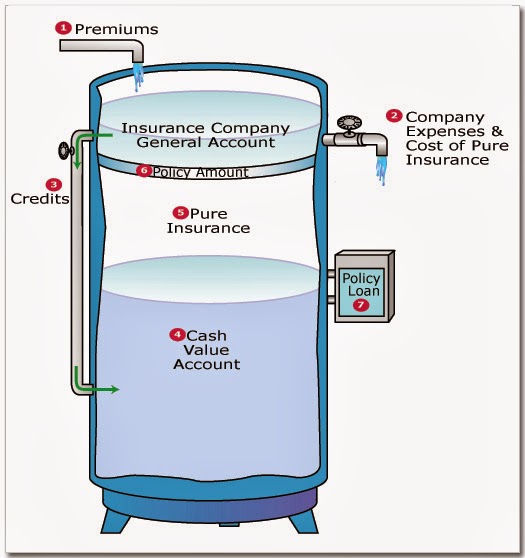

Whole vs UL

Donation/Charities,

Business Transfer,

Diversification,

Burial,

Tax-deferred and Tax-free,

Estate Planning,

Key Employee,

Account Receivable Loan,

Divorce Mandate,

Emergency Fund,

Education funds,

etc.Education funds,

See http://www.investopedia.com/articles/pf/07/whole_universal.asp

Monday, June 17, 2013

A Financial Bunker For Scary Times

A Financial Bunker For Scary Times

John E. Girouard via Forbes 6:30 PM ET

Suppose there was a financial instrument with a track record stretching back 140 years; that was

so solid it could survive the Great Depression intact; that earned untaxed interest at a competitive

rate; that could be borrowed against at will regardless of credit conditions; and that could be used

by individuals as well as major corporations and banks as a safe harbor during economic turmoil?

You'd call it a financial bunker for scary times, and you'd be talking about mutual whole life insurance.

This is not the life insurance that only pays when you die. Mutual whole life is the kind of

insurance owned in the good old days before the stock market began to boom in the 1980s and 1990s. Mutual whole life saw our elders through thick and thin,

and after several decades of being muscled aside by the allure of the stock market, it's making a comeback.

Mutual whole life policies have been an essential part of my financial planning practice for many

years. But I'm astonished at how few of the many investment advisers I meet understand how

mutual whole life policies work, or don't offer them to clients because they aren't sexy or new.

Mutual whole life fell so far out of favor in the 1990s that insurer Swiss Re-issued a report in 1999

headlined, "Are mutual insurers an endangered species?" Not anymore.

Mutual life insurance is making a comeback now that our speculative economy has blown up and

financial disaster is driving people away from risk and back to basics.

Mutual or "participating" whole life insurance is the closest thing to owning your own bank.

As New York Life has said in its ads, "We're Main Street. Not Wall Street."

The concept of mutual unsurance is rather simple, especially compared with the complex annuity products that were so popular until recently. And the benefits include all those listed in my opening paragraph.

Here, for the curious, is Mutual Whole Life 101, or The Life Insurance Policy for the Living:

--You Own The Bank: Mutual insurance companies are owned by the people who buy the

policies. These companies are the modern equivalent of mutual "societies" among European

trade guilds of the 1600s. Guild members pooled their money to help each other and their families

in times of sickness or death. Because mutual companies have no shareholders, they serve one

constituency--the policyholders. Mutuals have no need to report good earnings every three

months to justify a stock price, so there is no pressure for them to take on extra risk to make a profit.

--Your Premium Payments Belong To You: Unlike traditional term insurance, the premiums you

pay for your mutual whole life policy belong to you in the form of the accumulated "cash value" of

your policy. On top of that, the cash value of the accumulated premiums earns interest at a rate

set once each year. In 2008, Guardian Life paid a record 7.3% dividend interest, and those

earnings are untaxed! That's spectacular compared with a 10% decline in the stock

markets, bank CDs paying under 2% taxable, or money market rates under 0.1% taxable.

--You Can Borrow Back Your Premium Payments: Because your premiums "belong" to you as

a policyholder-owner of the company, you can borrow them back any time you want for any

reason you need, regardless of your creditworthiness. The death benefit of the life insurance will

be reduced by the amount you borrow, and you will lose the interest you would have earned. But

you can choose to pay the interest as you would for any loan, except you are paying yourself

instead of the stockholders of a bank. If you pay the loan back as well, the death benefit goes back up.

--Mutuals Offer Ironclad Guarantees: Few people realize that the insurance industry

was the one sector that made it through the Great Depression without a

disaster and with policyholders financially intact. The cash value and the death benefit are

guaranteed and tightly regulated by the states. That means your cash value is there regardless of

market conditions, and when you die your heirs will receive the full face value of the policy. |

While stockholder-owned insurance companies saw their values fall sharply (remember when

we taxpayers bailed out AIG?), the top mutually-owned insurers saw their book values remain

stable or rise.

--Even Banks and Corporations Buy Mutual Policies: One of the lesser-known aspects of

mutual insurance is that major corporations and banks buy policies on the lives of their

employees and use the cash value to fund employee benefits and as a safe harbor for working

capital. By some estimates Fortune 500 companies and large banks have policies covering some

5 million employees.

Instead of doing what banks say--put your money in our CDs at low rates so

we can turn around and lend your money out at a profit to us--do what banks do.

--Mutual Insurance Is One Leg of The Money Stool: Investing should be approached as a

three-legged stool. One leg is the money you need to live on in the near future (cash in the bank),

one leg is the money you invest for long-term growth (equities) and one leg is the financial bunker

you can retreat to when the rest of the world is falling apart and you can't sleep.

Life Insurance got our grandparents through the Great Depression, and it's going to get a lot of the people

through our current calamity.

John E. Girouard (www.johngirouard.com) is author of The Ten Truths of Wealth Creation, CEO

of Capital Asset Management Group in Bethesda, Md., and founder of the Institute for Financial

Independence, which provides investor education programs to financial professionals.

John E. Girouard via Forbes 6:30 PM ET

Suppose there was a financial instrument with a track record stretching back 140 years; that was

so solid it could survive the Great Depression intact; that earned untaxed interest at a competitive

rate; that could be borrowed against at will regardless of credit conditions; and that could be used

by individuals as well as major corporations and banks as a safe harbor during economic turmoil?

You'd call it a financial bunker for scary times, and you'd be talking about mutual whole life insurance.

This is not the life insurance that only pays when you die. Mutual whole life is the kind of

insurance owned in the good old days before the stock market began to boom in the 1980s and 1990s. Mutual whole life saw our elders through thick and thin,

and after several decades of being muscled aside by the allure of the stock market, it's making a comeback.

Mutual whole life policies have been an essential part of my financial planning practice for many

years. But I'm astonished at how few of the many investment advisers I meet understand how

mutual whole life policies work, or don't offer them to clients because they aren't sexy or new.

Mutual whole life fell so far out of favor in the 1990s that insurer Swiss Re-issued a report in 1999

headlined, "Are mutual insurers an endangered species?" Not anymore.

Mutual life insurance is making a comeback now that our speculative economy has blown up and

financial disaster is driving people away from risk and back to basics.

Mutual or "participating" whole life insurance is the closest thing to owning your own bank.

As New York Life has said in its ads, "We're Main Street. Not Wall Street."

The concept of mutual unsurance is rather simple, especially compared with the complex annuity products that were so popular until recently. And the benefits include all those listed in my opening paragraph.

Here, for the curious, is Mutual Whole Life 101, or The Life Insurance Policy for the Living:

--You Own The Bank: Mutual insurance companies are owned by the people who buy the

policies. These companies are the modern equivalent of mutual "societies" among European

trade guilds of the 1600s. Guild members pooled their money to help each other and their families

in times of sickness or death. Because mutual companies have no shareholders, they serve one

constituency--the policyholders. Mutuals have no need to report good earnings every three

months to justify a stock price, so there is no pressure for them to take on extra risk to make a profit.

--Your Premium Payments Belong To You: Unlike traditional term insurance, the premiums you

pay for your mutual whole life policy belong to you in the form of the accumulated "cash value" of

your policy. On top of that, the cash value of the accumulated premiums earns interest at a rate

set once each year. In 2008, Guardian Life paid a record 7.3% dividend interest, and those

earnings are untaxed! That's spectacular compared with a 10% decline in the stock

markets, bank CDs paying under 2% taxable, or money market rates under 0.1% taxable.

--You Can Borrow Back Your Premium Payments: Because your premiums "belong" to you as

a policyholder-owner of the company, you can borrow them back any time you want for any

reason you need, regardless of your creditworthiness. The death benefit of the life insurance will

be reduced by the amount you borrow, and you will lose the interest you would have earned. But

you can choose to pay the interest as you would for any loan, except you are paying yourself

instead of the stockholders of a bank. If you pay the loan back as well, the death benefit goes back up.

--Mutuals Offer Ironclad Guarantees: Few people realize that the insurance industry

was the one sector that made it through the Great Depression without a

disaster and with policyholders financially intact. The cash value and the death benefit are

guaranteed and tightly regulated by the states. That means your cash value is there regardless of

market conditions, and when you die your heirs will receive the full face value of the policy. |

While stockholder-owned insurance companies saw their values fall sharply (remember when

we taxpayers bailed out AIG?), the top mutually-owned insurers saw their book values remain

stable or rise.

--Even Banks and Corporations Buy Mutual Policies: One of the lesser-known aspects of

mutual insurance is that major corporations and banks buy policies on the lives of their

employees and use the cash value to fund employee benefits and as a safe harbor for working

capital. By some estimates Fortune 500 companies and large banks have policies covering some

5 million employees.

Instead of doing what banks say--put your money in our CDs at low rates so

we can turn around and lend your money out at a profit to us--do what banks do.

--Mutual Insurance Is One Leg of The Money Stool: Investing should be approached as a

three-legged stool. One leg is the money you need to live on in the near future (cash in the bank),

one leg is the money you invest for long-term growth (equities) and one leg is the financial bunker

you can retreat to when the rest of the world is falling apart and you can't sleep.

Life Insurance got our grandparents through the Great Depression, and it's going to get a lot of the people

through our current calamity.

John E. Girouard (www.johngirouard.com) is author of The Ten Truths of Wealth Creation, CEO

of Capital Asset Management Group in Bethesda, Md., and founder of the Institute for Financial

Independence, which provides investor education programs to financial professionals.

Subscribe to:

Comments (Atom)